Summary of key points:

- The luxury housing market has seen more dramatic changes compared to the overall market. Sales volume for $5M+ homes in San Francisco is down about 15% compared to pre-pandemic levels.

- The pandemic boom and stimulus money flowing into real estate were aberrations that skewed people's perceptions. We are now seeing a return to more normal appreciation rates of 1-4% annually.

- Location has a big impact. Areas farther from downtown San Francisco (Sunset, Richmond, Sea Cliff) have fared better than downtown and South of Market. Proximity to urban issues has driven people to more suburban areas.

- Turnkey homes that need no renovation are most desirable now due to uncertainty around construction costs. Homes must also be well-presented and competitively priced.

- Inspection contingencies allow buyers to renegotiate prices more now than during the frenzied market. Less competition gives buyers more leverage.

- Threats remain including inflation, debt coming due for commercial real estate, and lag effects from interest rate hikes. But positive signs like tech hiring and return of tourism signal a bottom may be near.

- Marin County has been more resilient as wealthy SF buyers move there. Worst case 10% price drops versus 20% in SF.

- Overall the market seems to be cautiously recovering from the pandemic aberration back to normal appreciation rates. But risks remain so continued caution is warranted.

—

Market Update Interview - August 2023

Question: I just wanted to get more context and an on-the-ground perspective on what's happening in the luxury market segment. I want to separate some of the fact from fiction or people's perceptions. Some of the data shows home sales as a whole, and luxury home sales more drastically, falling starting last year.

I want to understand a bit about what you're seeing on the ground, whether you're seeing commensurate pricing discounts alongside it, and what some of the causes of that shift have been. Additionally, what has been the impact of some of these macroeconomic changes amongst buyers and sellers in this segment?

Answer: Sure, those are big questions, but I'll do my best to convey my understanding of what I see going on out there. I think more now than ever, the question of what's the market doing or even the more specific question of what are different market segments doing, is almost the wrong question. I think the right question is, what house do you own?

Because certain houses are not affected by this downturn at all, while others are affected up to 20% [discounted] if you're in San Francisco, which is the worst-case scenario, and in Marin, about 10% is worst case.

So there's a lot of possibilities in between, right? Zero depreciation to -20%. And so it really is house-specific. I think you asked a question about what type of housing characteristics are more desirable right now in this market condition.

I think it really comes down to, is the home turnkey, i.e., can you just move in and unpack and start living, or do you have to do a bunch of stuff to it first? That's really important right now because construction costs are a big unknown. The needles have been moving in so many different directions with lumber, drywall, flooring, and all these things that go into a home. For people to actually put together a renovation budget is more difficult than it has been in years past. So running the calculus on that is a turnoff in a lot of ways. People are desiring turnkey homes, but that's not enough.

It has to be well presented, competitively priced, and in a desirable area to fare better than the competition. Buyers are able to be more picky right now than they have been able to in years past. So, there are a lot of dynamics going on right now, but I think the main takeaway, at least from what I'm seeing out there, is that it's very house-dependent right now.

—

Question: Area-wise, where have we seen changes? I've written in the past that downtown has been struggling for a variety of reasons, including a lack of amenities and traffic. We've seen a downward pricing trend in the condo market, and I think that's across all segments. Single family homes have been less impacted by that, of course. Where are the different geographical divergences between areas with a particularly strong market versus those that have experienced more softness?

Answer: Following the pandemic, a new trend emerged in San Francisco, and this very well may be true for other densely populated cities as well. What we saw was, if you can visualize concentric rings radiating outward from downtown and the financial district, the closer you were, the more negatively affected your property value was, and the further you went out, the better.

For example, last year in 2022, the Sunset was arguably the hottest neighborhood in San Francisco. It was just absolutely going bonkers. Neighborhoods like Sea Cliff, Lake Street Corridor, and the Richmond District were all neighborhoods that, pre-pandemic, were often thought of as being too far away. Post-pandemic, people are desiring more distance between themselves and downtown.

We've seen a big spike in values in Jordan Park and the Laurel Village area, which have become even more highly desirable. Presidio and Pacific Heights have both maintained their place in the market, which is at the very top.

Unfortunately, the neighborhoods closer to downtown have suffered the most. I do think a recovery is underway, and we can get into more of that if you want, but the neighborhoods close to downtown that took the hardest hit would be South of Market, parts of the Mission, Hayes Valley in some areas, and some of South Beach, Mission Bay, and the waterfront area, especially where the new high rises are. Those markets have not fared as well as the more outlying areas, and I think that's due to a new way people are living.

I also think a large part of that dynamic has to do with the state of downtown and the financial district right now. It's just not a super desirable place to be right now, and people don't want to wait around for it to get better. They want to live their best life now, so they're moving to areas where they can get that immediately rather than having to wait for a renaissance.

—

Question: It's interesting you mentioned this, kind of like circles or the distance away from downtown. Have, we'll say, urban concerns created, I guess, more of the desire for folks who've been here a long time to hit the suburbanization trend, look for properties either in Marin or down on the Peninsula or something like that. How have you seen the impact of some of the concerns around some of the situations downtown and perceptions of San Francisco writ large impact people's decisions around where to locate?

Answer: Sure, I don't think it's any big secret that the state of San Francisco or the rough patch it's been going through, struggling with some of these social issues, has turned off a lot of people and they have decided to move not necessarily out of the Bay Area, just to different parts of the Bay Area. And while those folks may still commute into downtown or the financial district, they are choosing to live in other communities.

I think that's a trend that has accelerated over time. People who lived in San Francisco in the seventies and eighties will say it's not as bad as it was then. San Francisco has always had this characteristic. If it's your first time experiencing it — and therefore in stark contrast to how the city was a few years back — it’s likely that it’s the contrast that's bothering you and that's the reason why you're leaving. But people who've been through many cycles in the city know that it's a boom-bust town.

And when it's booming, it's amazing. When it busts, well, it's got an ugly side too, and that's what everyone has to live with for a while. I also think the rate at which information travels now is much different than prior cycles. Our awareness of it has definitely been put on steroids in terms of pictures and videos and all that stuff being shared about the blight. If cell phone cameras/videos existed back in the 1970s, and we had all that record, we could compare the two and it probably would have a very similar look and feel— maybe even worse.

These cycles are natural for any city. For San Francisco, I think it tends to, because of the weather, where it's located, and our tolerance for a lot of different things, attract that type of activity. During a downturn, it becomes the face of the city. And that's what it's experienced over the last couple of years. But I do think a lot of the locals have had enough. The city has lost out on a lot of tax revenue and conventions. It's really starting to hit them in the pocketbook, and I think that's ultimately what's going to get the attention of our leaders. And, hopefully, they can start cleaning things up.

—

Question: Have we seen any divergence among the different market segments?

It seems the luxury housing market has dipped a bit more strongly because of the smaller sample size, so to speak. But has it been going in line with the rest of the broader market, or have we seen more dramatic changes depending on the market segment?

Answer: I do think your observation is correct. The higher you go up the property ladder, the more susceptible those homes are to wild swings in value. This is not just true during a downturn, but also during a boom. As a former real estate appraiser with 20 years of experience, I am very data-centric.

When I analyze homes that are worth 10, 15, or 20 million dollars, the error bars can be in the millions. You're like, "Yeah, I think it's worth 20, but it could also be worth 23 and it could also be worth 17, based on the model.” And so, you have these gigantic swings in value the higher you go up the property ladder. And it’s mainly because the market is so thin at those levels that you literally one buyer and one seller creating that market for that house. As opposed to an $800,000 single-family home where you have one seller and 15 buyers who are creating that market, and 15 buyers have 15 different opinions and they settle on a single prevailing party. The data point for that is so much more reliable because you had 14 other people who were also interested in buying it. So you get a sampling as opposed to something way up the property ladder where it's just one-on-one.

That's just the natural way the market works, for that reason, when we have these big market changes like we're going through right now, the properties that have the biggest error bars are also going to have the biggest changes in value. So that, to me, is just a natural function of the way the market works at different price points.

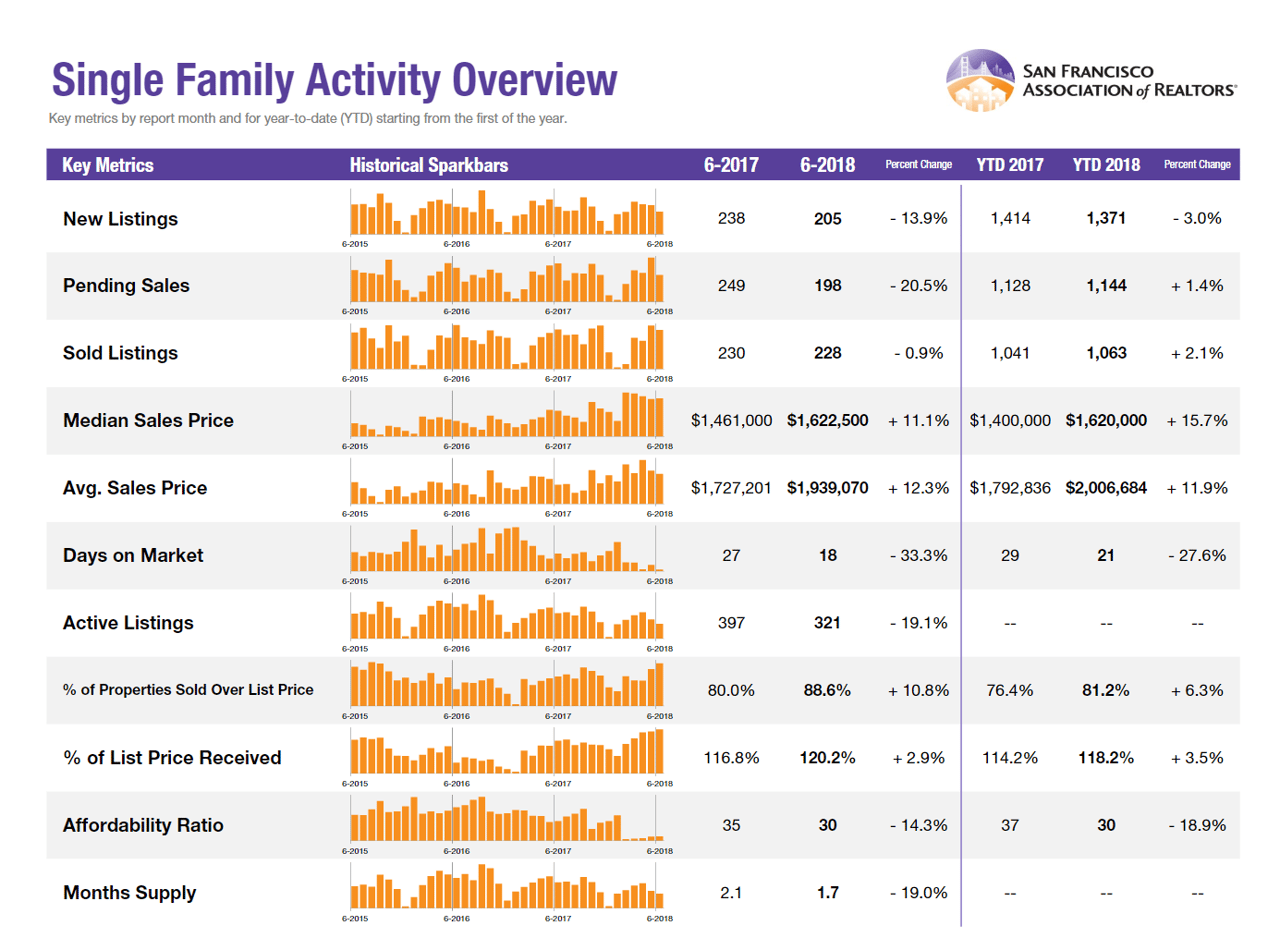

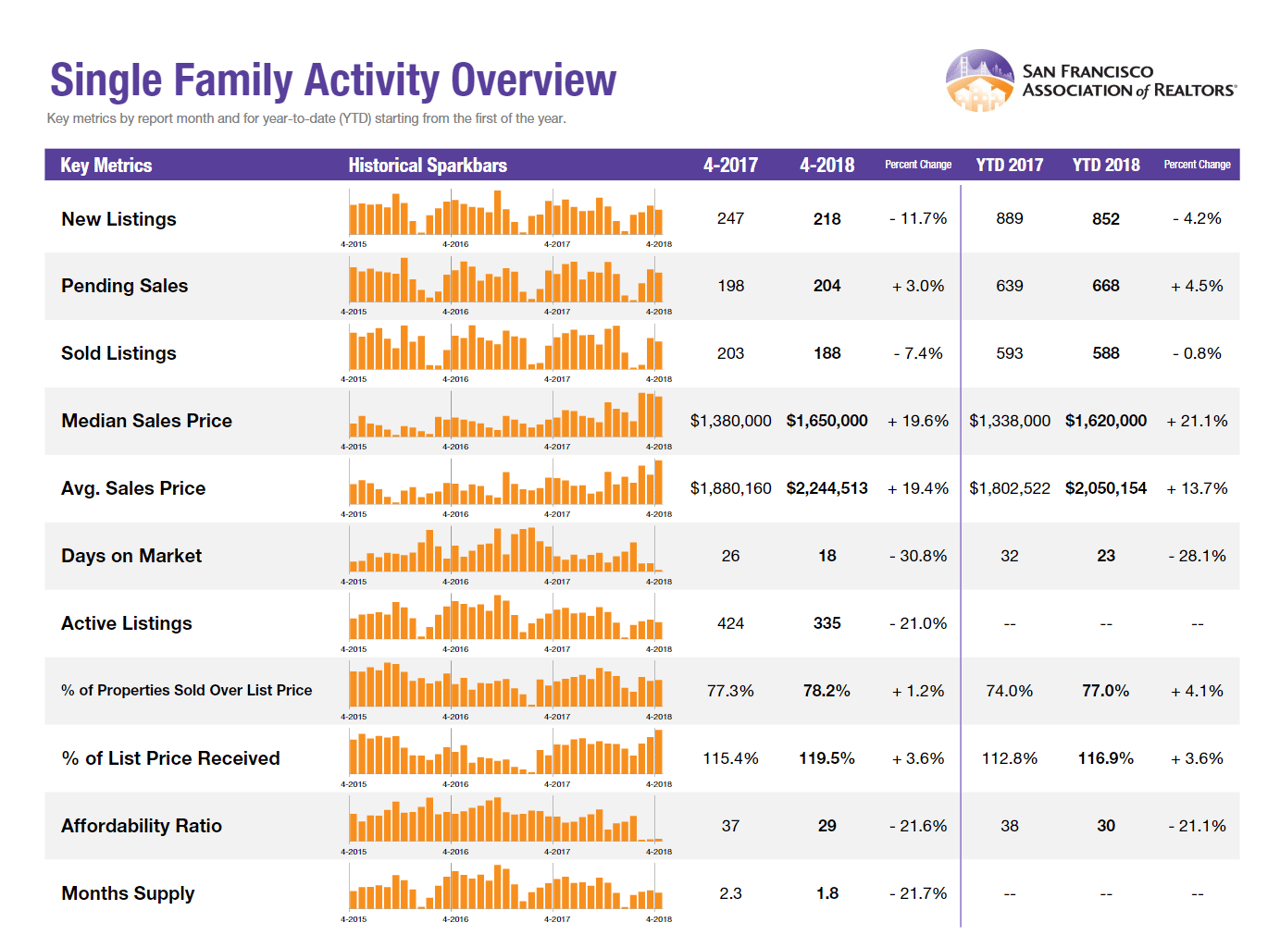

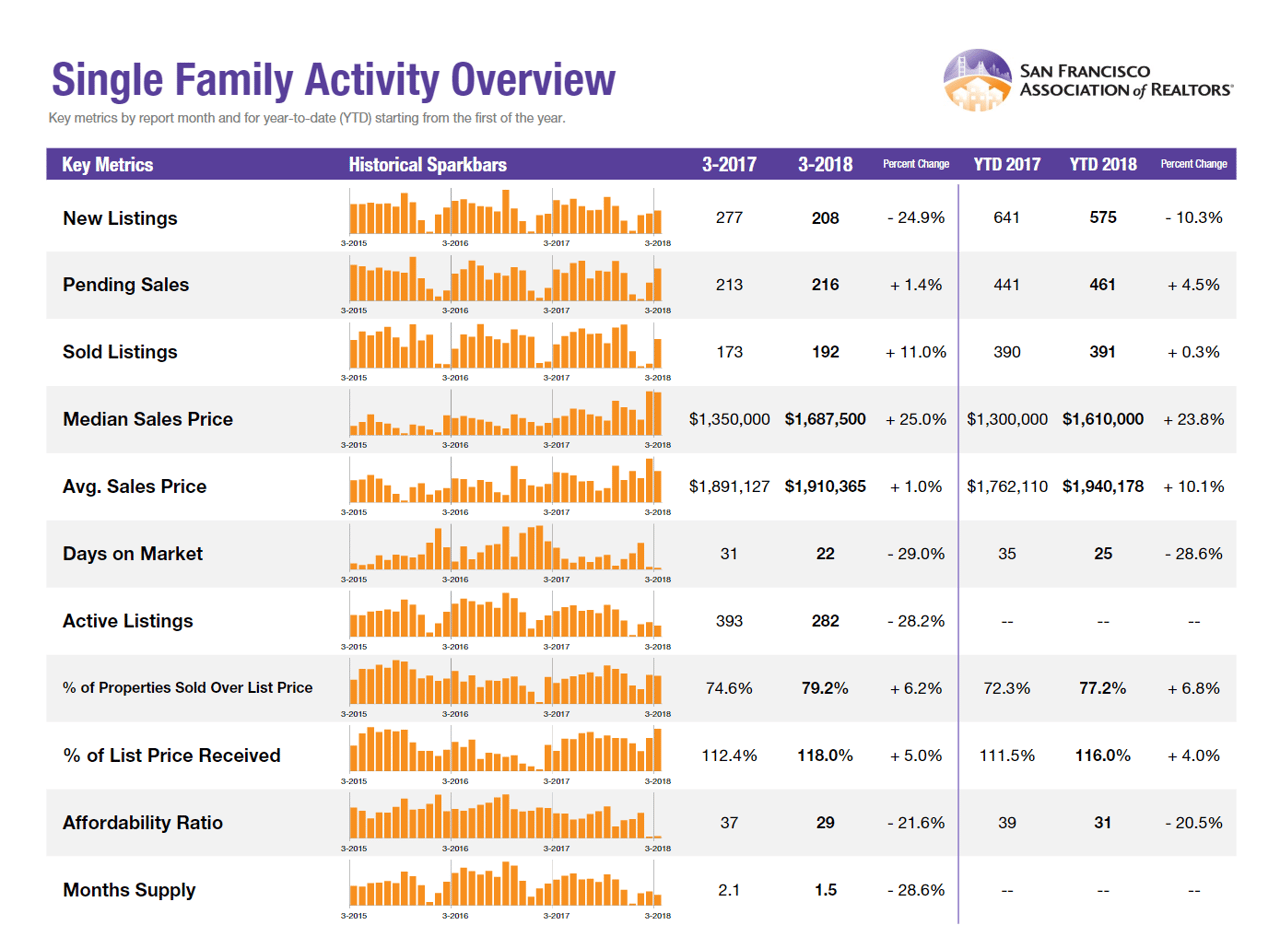

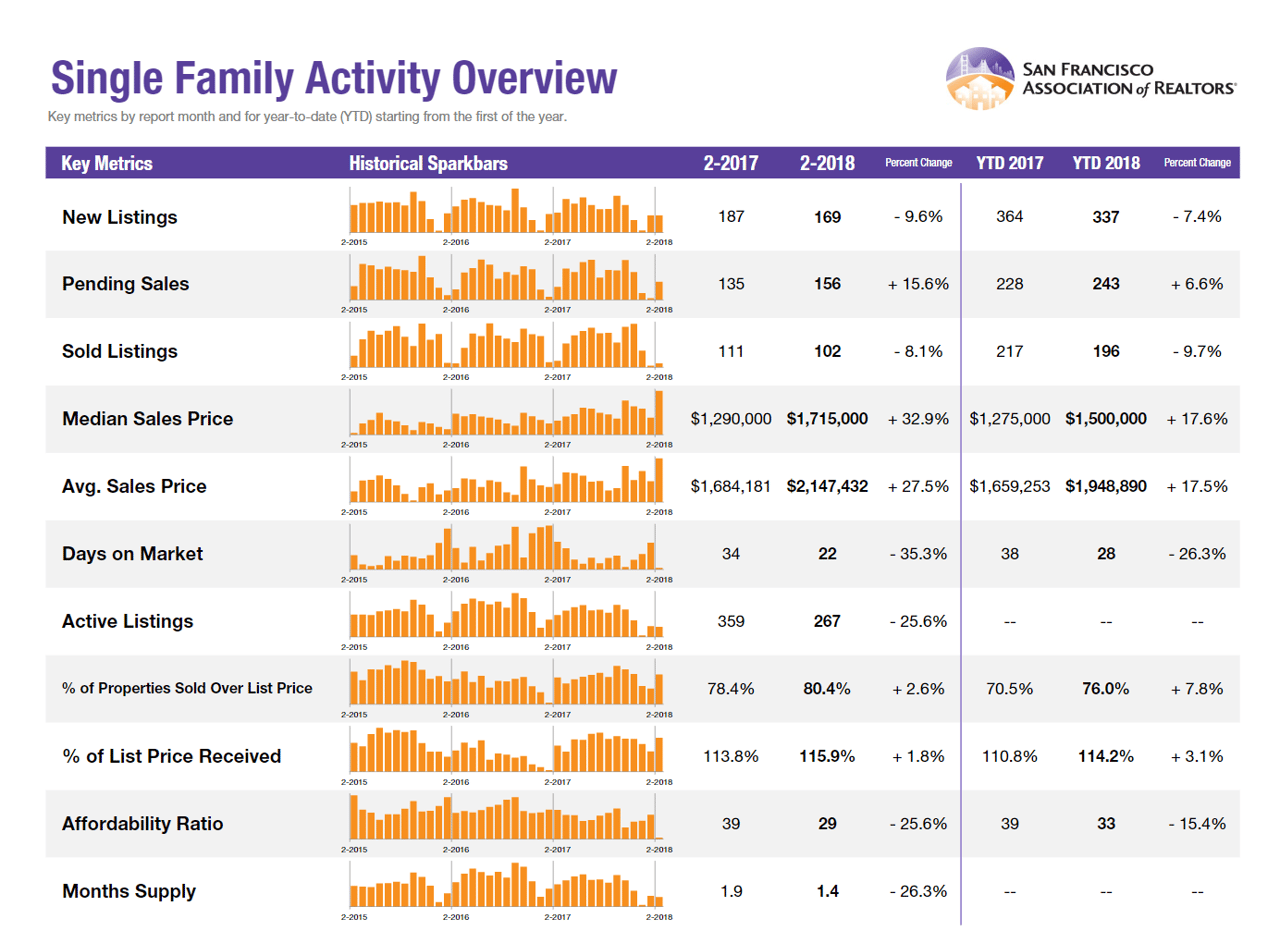

I pulled some numbers to see what the sales volume looks like for $5 million properties in San Francisco, trading from January 1st through August 22nd of each of the last eight years. In 2023, we've had 42 trades, compared to 97 trades in 2022 and 114 trades in 2021. In 2020, which was the pandemic year, we only had 30 trades, but the market was shut down for three or four months.

If you go back pre-pandemic, the $5 million-plus market was averaging around 45 to 50 trades a year [YTD]. Currently, we're at 42 trades YTD. So, while activity is a bit depressed, it's not as bad as the media makes it out to be. It's more like a 15% decline in activity compared to pre-pandemic levels if you factor in inflation and market movement.

The pandemic years were such an aberration that the data could be considered outliers. The amount of stimulus put into the economy was unprecedented, and that money flowed into many different places, including real estate. Comparing the current market to pre-pandemic times, it's not a full capitulation. The worst-case scenario for a property in San Francisco is a 20% decline in value, but the best case could be a slight increase in value due to desirability. There are many possibilities in between.

—

Question: I think that historical context is important just because I think maybe perceptions are a bit skewed because of the last couple of years and how much of an aberration that was to typical trends.

But I'm actually curious if the aberration has sort of skewed people's perceptions on where they think valuations are? How has that impacted people who have short memories and aren't necessarily looking back at all this data?

Has there been a mismatch between their conception of where things just were, maybe two years ago, versus where things are now today?

Answer: Yeah, I think there is. It's like when you give a kid a toy and then you take it back, right?

The kid's used to the toy, now they want the toy, they want to keep playing with it. But you took it back. I think the psychology is ‘we're going to get our toy back. It's going to come back. I'm just in a timeout right now, or I'm grounded. It's still there. It hasn't gone away.’

So I think the psychology is— even for people that bought during the frenzy— and I myself am included, I bought one of my houses in 2020— I think the psychology is that there's a dip and we're going to go through the dip, and then we're going to come out of it, and then we’re off to the races again.

Maybe off to the races isn't the right term because I do think, and this is projecting forward a little bit, while I do think a recovery is just getting started right now, I'm not expecting hockey stick growth coming out of this thing. I'm expecting more subtle moves, maybe even flat-lining for a little while before the growth comes back.

It still is very house specific, but generally speaking, you're probably looking at 1% to 4% appreciation over the next 12 months depending on what property you have. As opposed to the last year and a half, where you've been looking at depreciation.

So I think the bottom is near. I'm knocking on wood as I say that because there are some pretty big threats still out there looming. And it remains to be seen how those will play out. The big looming threats that exist to the market right now are— first, inflation. If inflation comes back and those numbers start going up again, then I think that's a game changer. That could mean the Fed is going to have to keep tightening.

And interest rates are going to go far higher than any of us had ever imagined. And that will be extremely bad news for not just the real estate market, but probably for the financial markets as well. So that's one big threat.

I think another big threat is all the debt that is coming due particularly on commercial real estate and multifamily.

There's a report that just came out by Trepp Commercial Real Estate out of New York. They published a well-written report with heat maps and all kinds of geeky stuff that I like. They discussed San Francisco and how crime relates to the success of businesses, the number of businesses, and the closure of businesses.

In that report, buried at the end, they went through a bunch of buildings that are in distress right now in San Francisco. Basically, because the tenants have left, the landlords are now upside down in their debt service, what they owe on these buildings. That's a messy situation. So if rates don't start coming down in the near future, that is a massive threat to the entire economy. Commercial real estate could take the whole thing down. And part and parcel of that is multifamily, as multifamily is also considered commercial.

So all that math has changed for the folks who own those buildings and the debt that they hold on it. And if you combine that with tenants vacating, companies going bust, it could get really ugly really quickly.

The last of the three looming things is the lag effect itself. We don't really yet know the effect of this rate hiking cycle, which if I'm not mistaken, was the sharpest rise in history and right now we're sitting at, I think it's 20 or 22 year highs for mortgage rates.

We don't really know the effect of all that in real time. It will take months to play out and so there are some threats looming, but I do feel like I can just tell you anecdotally the second half of 2022 was probably the quietest I've had in my whole career. And we weren't panicking, we were actually resting because we had been sprinting for the previous two years. But when that started to bleed into the first half of 2023, which was also pretty paltry, we were like, okay, when are these deals going to start happening? When are people going to start moving again?

I think just starting about a month ago, there's a real palpable sense that people now think that the bottom is in. And because people can see that rates are potentially going to be coming down in 2024, and this may be their last opportunity to A) get a property at a pretty decent price, and B) not have to compete with 10 other people.

Those who have this view are jumping into the market and they're all jumping in at the same time. And so just in the last week I've gotten four properties into contract, which is fantastic compared to what we've been experiencing the prior year.

Things definitely seemed like they're turning a corner. And even if you look at Chair Powell's Fed meeting back in June, he even remarked in that meeting— if you watch the tape— that he thought the real estate market had put in a bottom.

So those are all really positive signals. San Francisco-specific stuff like AI companies moving into SOMA and the financial district and downtown. I think those are all, if you want to talk about that, we can. I think that's all also positive signals for our market.

—

Question: We've been talking a lot about San Francisco. I know you guys are also active in the North Bay. Are similar dynamics at play up in that market as well, or are we seeing a little bit of a divergence there?

Answer: Yeah, I think there's a divergence. I think that, and I'm just speaking about Marin County in particular, it has been the recipient of many wealthy people who have left San Francisco but wanted to stay in the Bay Area.

So they've had an influx of people, especially wealthy people who have moved in, and the city has lost those people and lost that tax base unless it was replaced by someone else coming in. I think that is one of the reasons the Marin market has fared better than the San Francisco market during this particular downturn. It's been the beneficiary of migratory patterns and, earlier, I mentioned that 20% down was the worst case in San Francisco and Marin. Your worst case scenario is more like 10% down. But most houses in desirable communities in Marin that are turnkey haven't gone down at all.

Marin also has different towns, different school districts, and it's very market-to-market. There are little micro trends everywhere, and you have to learn about all the different towns and how they behave from a market standpoint.

But overall, it's been much more resilient during this downturn than San Francisco.

—

Question: One thing you mentioned is you have essentially very small groups, single buyer, a single seller, maybe, two buyers and a seller making the market. Has that put a little bit more leverage on the buy-side to be able — particularly in that segment where they're less in need of financing— they have a lot more liquidity to put down? Do they have a little bit more leverage in the way that they're able to dictate some of the terms and the negotiations— what are we seeing on that front?

Answer: Sure. And I think this is true for any price point, but if you're a cash buyer, cash can be worth anywhere from 1% to 5% of the purchase price, depending on the seller's appetite for risk.

So what I mean by that is, let's say you have a $10 million home. One buyer's getting a loan, the other buyer's cash. The person who's cash may be able to offer 1% less than the other buyer and still win— still get the house. Because the seller just simply doesn't want the added complexity, the added unknowns, of having a lender involved. 1% all the way up to maybe 5%. It depends on the seller's appetite for risk. If the seller's very risk averse and they're like, "I don't care. I want to sleep at night knowing the deal's done and that the money's in the bank" .. so, I'm willing to even take 5% less than a like-kind offer that's getting a loan.

So cash does have meaning. It just depends on the seller how much meaning it has. The other thing that I'm seeing right now, and this is true across all price points, is that buyers are enjoying a lot less competition, and in many cases, no competition.

And if you're a buyer and you're not competing with anyone else, then you can write in any old contingency you want, and the most important contingency for renegotiating a sales price is the inspection contingency. So if you write in an inspection contingency and then you go and do a bunch of inspections and you find things that were previously unknown and the inspectors give you dollar amounts for those things, you can go back to the seller and renegotiate your previously agreed-upon sales price.

That is a trend that's happening all the time right now. And that is just not something you see during a hot market. During a hot market, the seller's in the driver's seat and the seller has five offers and the seller will accept the one that's not only the best price, but usually the one that doesn't have any contingencies because the contingencies leave the door open for renegotiations.

So we're in a market right now where sellers should not be counting on their agreed-upon contract price to actually stick until the inspection contingencies or any other contingencies have been removed. Then they can know what they're actually getting for the house. That's a new dynamic. And look, that's just normal real estate. That's a normal situation in other markets across the United States, even when the market's hot, that's how things operate for you. But in San Francisco and Marin— when things get hot— there are so many more buyers than there are sellers that you basically never get to write in contingencies.

So that's not a new dynamic, it's just a cyclical dynamic.

—

Question: Interesting. I think we hit most of the things that I wanted to talk about. Was there anything else that you think is pertinent?

Answer: Yes. As I mentioned, I am a former appraiser and data geek. I basically spend half of my life in Excel running different types of pricing models, neighborhood models, all to provide my clients with the best information I can. I will tell you the most important data point I've looked at in the last three weeks was on the Golden Gate Bridge.

I was driving across and I saw a double-decker tourist bus, one of those SF Tours buses, the double-decker red kind. And it had a big sign plastered on it and it said "Drivers Wanted - Now Hiring - CDL required." I got chills when I saw it. Because that, to me, was the most important data point I had seen in regard to anything San Francisco related in a while.

And I know it's anecdotal and it even sounds ridiculous, but I got chills when I saw that sign. Because if I'm reading this correctly, I'm pretty sure that means the tourists are starting to come back and these buses need more drivers and they're growing again.

These companies had to get really lean for a while -- everyone's had to get lean. But to see that really gave me hope. And I think that, based on the homes I put in a contract in the past week and how unbelievably busy I am again, after a year of really paltry activity.

All those things are conspiring -- Chair Powell's comment a couple months ago back in the June Fed meeting -- all that stuff is conspiring for me to start being really hopeful and cautiously optimistic about the market.

We did talk quite a bit about looming threats. And those are always in the back of my mind and I definitely have my head on a swivel for those things. But in general, this is the most optimistic I've been in a while. So yeah, I think things are starting to look up and there's a big technology boom coming in terms of AI. But maybe that's a topic for another day...

—

Question: I was looking at homes in this sort of segment and then just reaching out to some of the listing agents on them. I did a little research on some of these folks. You seem to have a lot of experience, and like you said, I thought it was a valuable perspective. I read your bio and saw you're a former appraiser too. I think it's a good perspective to be gleaned. I very much appreciate your particularly analytic approach to talking about this.

A lot of times when I talk to brokers and stuff, there are feelings in the air, it's nice to have some data analysis behind your perspective. If you could share with me the numbers you pulled for the $5 million plus sales over the years.

Answer: I’ll send you over a couple tables that I ran, and one interesting one is the sales price to list price ratio for sold listings above $5 million. Year to date and during the peak, homes over $5 million were fetching 104% of their asking price.

Right now, year to date, it's 96% of the asking price. That's an 8% swing, which is not trivial. If you have a $5 million home, that's $400k. But it's not capitulation, and it's not sky's falling type stuff. If you look back once again, pre-pandemic, which I'll include in the table I sent over, the numbers are usually right around a 100% percent.

So the sales price list, price ratio is an important metric I look at to see if sellers are getting their full ask, and this is a market where they're not. But it's not 82%, it's 96%.

Most of the charts I look at, the pandemic boom almost looks like a heartbeat on an EKG. There’s a big spike up and then a dip, and then back to baseline again. We went through the spike up. We're going through the dip now. I think we're returning to baseline. And hopefully the heart keeps beating!

Disclaimer

NFA / DYOR - Not Financial Advice / Do Your Own Research

Information provided herein is for informational purposes only and is subject to change without notice. This publication does not constitute, either explicitly or implicitly, any services or financial advice by Artemis Real Estate. Information provided is not guaranteed, and Artemis does not guarantee the accuracy of any information obtained from a third party.