Greetings and welcome to the Spring 2023 installment of the Artemis Advisor!

This update is packed with info, so we’ll jump right in. But first, a special thank you to all of the compliments we receive on the newsletter. It’s great to hear that our original content is valued and the compliments help keep us going, especially when writer’s block sets in!

Market Update: How close to the money printer are YOU?

No need to sugarcoat things - it’s a tough environment at the moment. Not as bad as ’08/’09, but tough nonetheless. The failure of First Republic Bank has rattled the markets and left a big hole in local lending. Back in our October 2022 edition, we predicted that 2023 would be “The Year of the Balance Sheet”, stating that “…a big spotlight will be shone upon corporate, institutional, and household balance sheets. If a balance sheet is weak, it will be exposed.” Obviously we did not predict the failures of SVB or FRB, but we got the broad strokes correct, and the balance sheet concept will continue to play out (and perhaps become even more pronounced) as we get into the latter half of the year.

The challenges of the current market condition highlight the Cantillon Effect. If you haven’t heard of it before, the Cantillon Effect is an economic thesis by Richard Cantillon, a French economist from the 18th century. The thesis describes the uneven distribution of new money created by central banks and its impact on the economy. When central banks create new money, either through quantitative easing or other monetary policies, this new money doesn't immediately spread evenly throughout the economy. Instead, it first goes to certain sectors, institutions, or individuals before trickling down to the rest of the economy. Those who receive the new money first-- those standing closest to the money printer-- benefit the most, as they can spend or invest it before the price levels in the economy rise due to inflation. This advantage allows them to acquire assets or goods at lower prices before the new money drives up prices.

Who exactly is “standing close to the money printer”? Commercial and financial institutions, large corporations, government entities, high net-worth individuals, the real estate sector, venture capital and private equity, stock market investors, export-oriented industries, and virtually anyone holding assets. This is important because when money gets vacuumed back out of the economy in a tightening cycle, like we’re in right now, the people that benefitted the most are now the ones feeling the most pain. And there you have it. The current market will actually reveal to you how close you’ve been standing to the money printer. Those of us in the real estate sector can definitely feel the pinch, and we’re sure many of you can as well. Similarly, and on a larger scale, certain regions are revealed as having an outsized benefit during periods of monetary expansion. The San Francisco Bay Area is one of those regions, and as you’ve probably felt personally (or read in the headlines), we’re feeling more pain than many other regions as money gets pulled back out of the system.

Despite local bank failures and money being sucked out of the economy, our local real estate market plugs along. It’s a mixed bag - but in general - it’s better to be a buyer right now versus years past. While inventory remains scarce, buyers are enjoying less competition (and in many cases zero competition), are oftentimes able to write contingencies into their offers, and more negotiating is taking place. Depending on your individual situation, the property in question, your financing options, and most importantly your projected hold-time, now could be a great time to buy property if you believe in our region long term (which we most assuredly do!)

Bay Area buying opportunities rarely come along, and when they do, are fairly short-lived. As soon as the Fed begins cutting rates, which could be anywhere from 6-18 months from now, the market will regain steam and said opportunities will have vanished. Stay tuned to our newsletter as we’ll most certainly be keeping tabs on when this shift occurs.

Here at Artemis we’ve been busy with our listings and buyers. We have a wonderful off-market listing available— a Park Avenue-style Pacific Heights condo at 1896 Pacific #702 offered for $3,885,000 along with a few other offerings as well. Next week we’ll be launching a resort-style gated property in San Rafael - so stay tuned! And we are happy to report that several of our listings have recently gone into contract or sold, including 99 Via Los Altos in Tiburon for $6,950,000 and 3709 25th Street in Noe Valley, which is now Pending. See Our Properties for more details. Our buyers face a mixed market- some homes are competitive and others aren’t.

You may have recently heard that State Farm General Insurance Company, State Farm’s provider of homeowners insurance in California, ceased accepting new applications, including all business and personal lines property and casualty insurance, effective May 27, 2023. State Farm made this decision due to historic increases in construction costs outpacing inflation, rapidly growing catastrophe exposure, and a challenging reinsurance market. From InsuranceNewsNet, “With the five years of intense wildfires and losses that we’ve had, we pretty much lost all our underwriting profit that we had from the last 20 years,” said the institute’s Janet Ruiz.

Credit and insurance availability is incredibly important for a functioning real estate market. Recent disruptions to both have added significantly to deal complexity and viability. It’s another sign of the times and a developing story we are tracking through lived experience. And that leads us to this month’s prediction…

Monthly Prediction: Insurance Pre-Approvals

If you’ve ever written an offer to purchase a property, you’ve probably been counseled that you should have a pre-approval letter from a lender (or banker letter confirming cash) accompanying the offer. With the recent news of State Farm and All State pulling out of CA (for homeowners policies), insurability has become a sticking point in many real estate transactions. We predict, at some point in the not-too-distant future, that offers from buyers may start having pre-insurance letters attached. This would give a seller confidence that the buyer has done some diligence in investigating which companies will underwrite a policy on the property in question. If so, an offer would now consist of the purchase agreement, a lender pre-approval (or banker letter if a cash purchase), an insurance pre-approval, signed disclosures (or disclosure acknowledgment), and an optional personal letter (which are waning in popularity due to fair housing guidelines, but that’s a topic for another day).

Another way this could manifest would be for sellers to preemptively provide insurance pre-approvals in their disclosure package. Either way, if insurability remains a significant wildcard, we suspect one of these trends could emerge.

In California, the FAIR (Fair Access to Insurance Requirements) Plan is available as insurance of last resort and can offer up to $3 million coverage for homeowners. It is a state-mandated program that provides access to insurance for individuals who are unable to obtain insurance in the regular market. But since it caps at $3M, anyone using it for property above that threshold will be underinsured.

Insurance and lending are two vital components of any real estate transaction, and both are experiencing a time of turmoil. These disruptions add significant complexity to deals. Proper counsel for this rapidly changing landscape is essential for real estate success and risk management, so be sure to get in touch if we may be a source of information for you or your friends/family/colleagues.

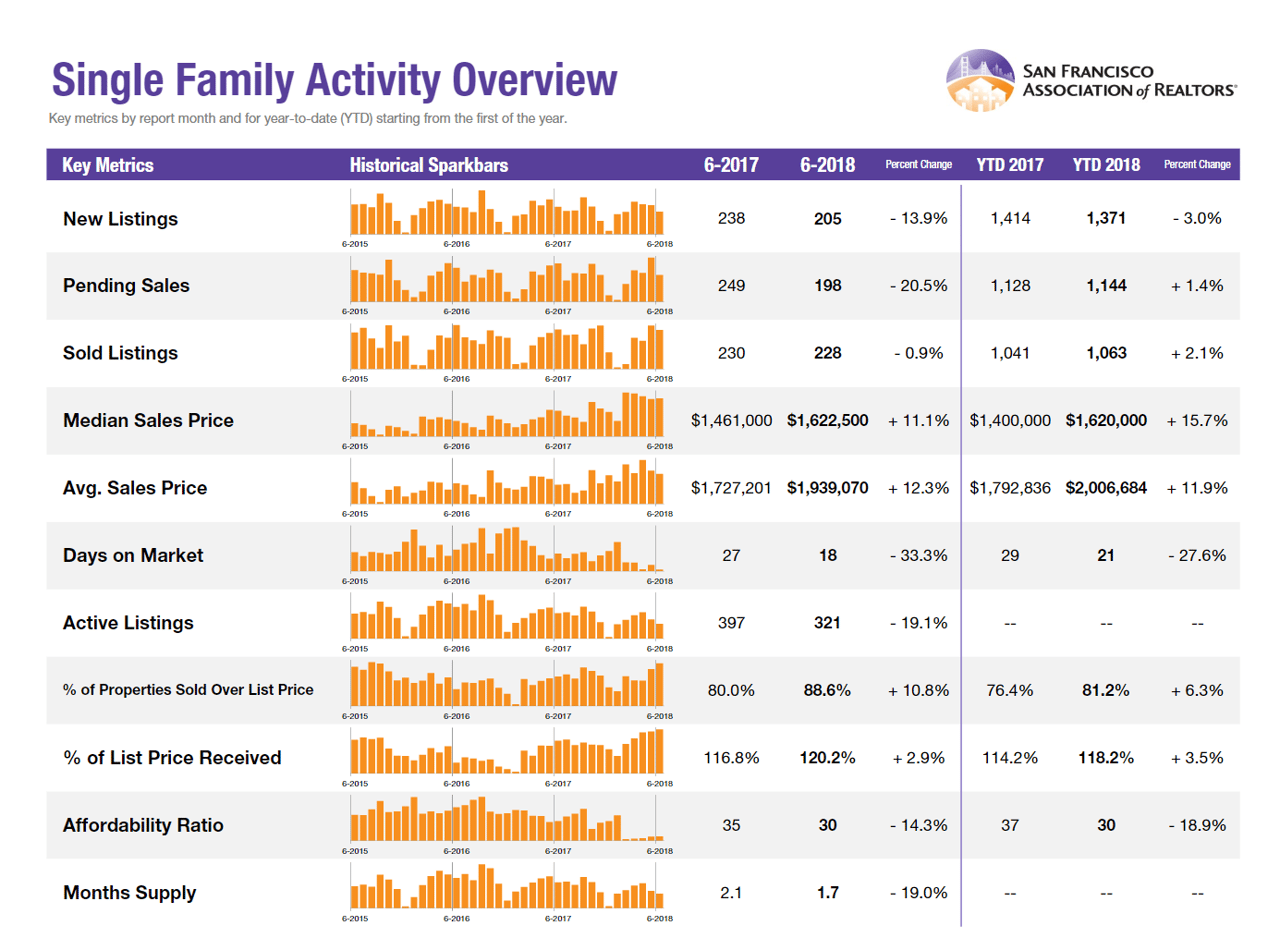

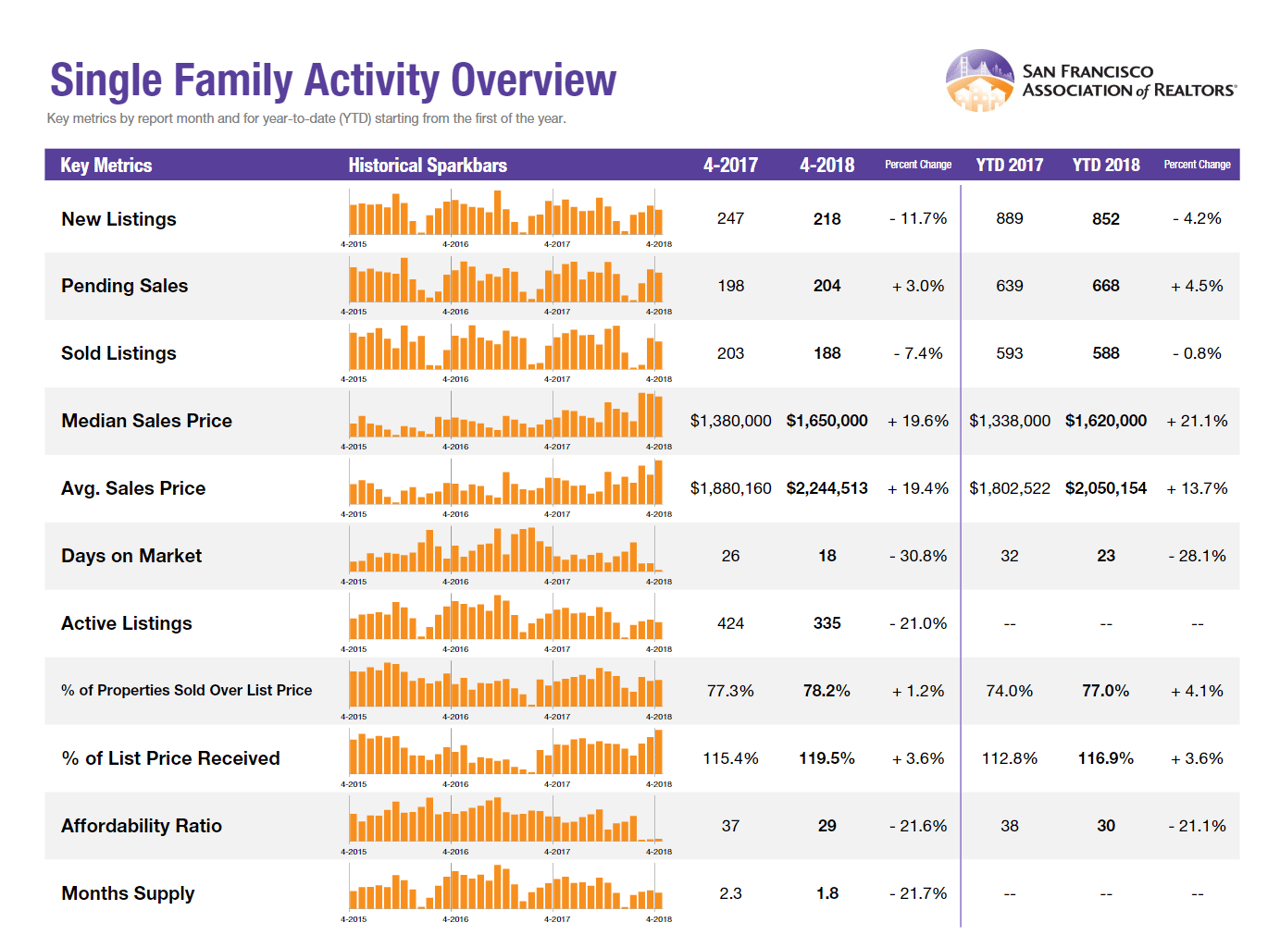

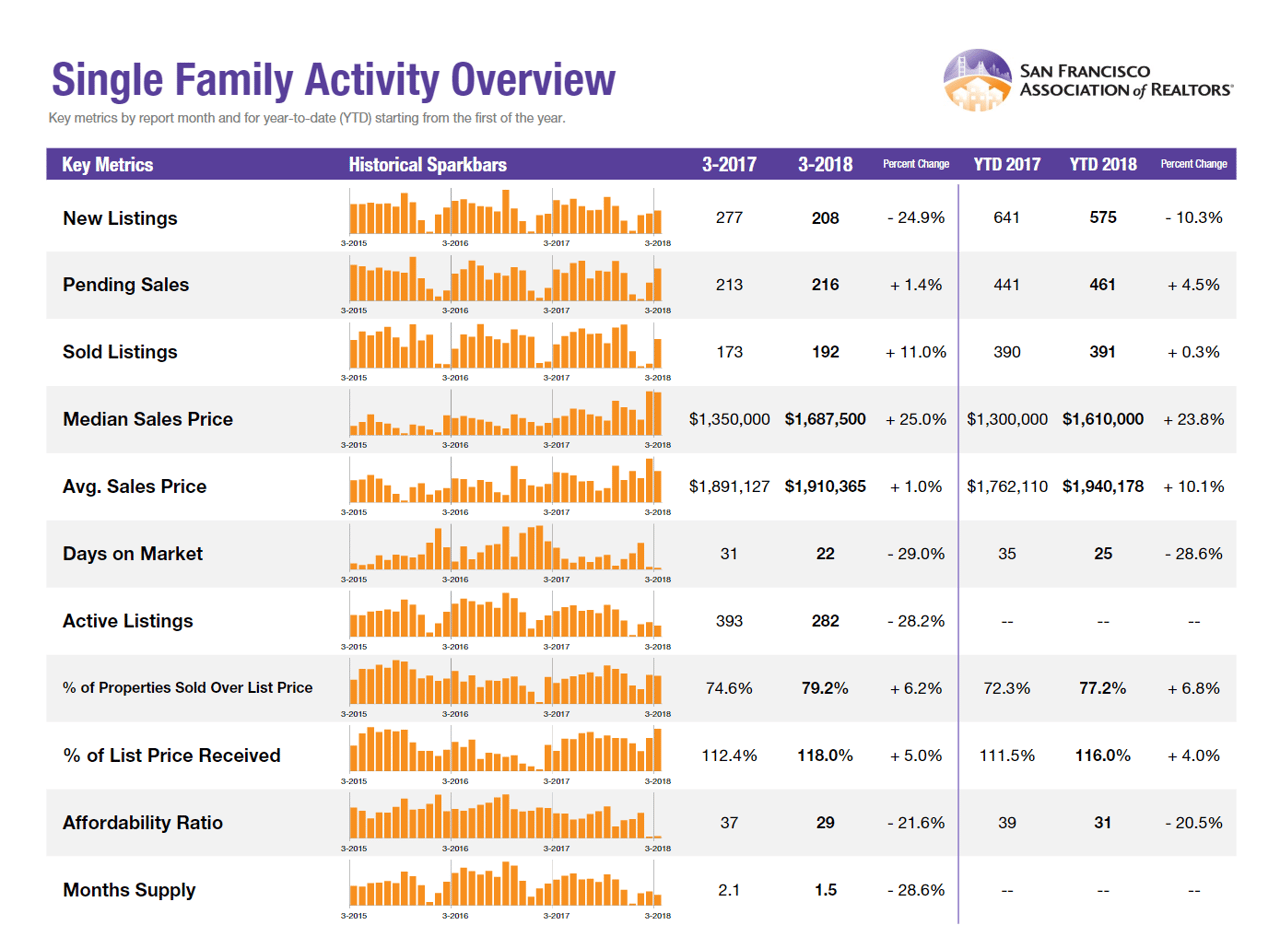

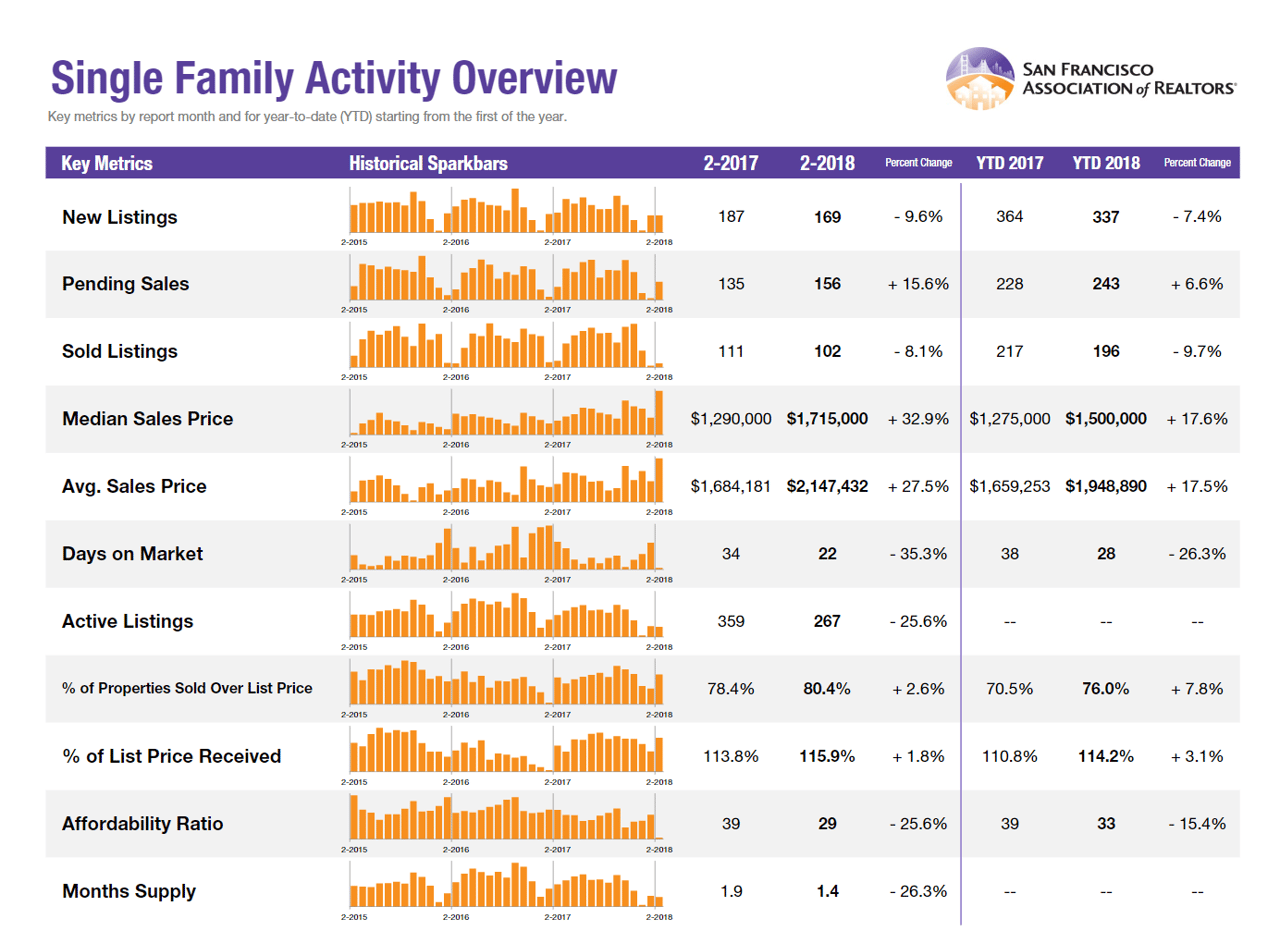

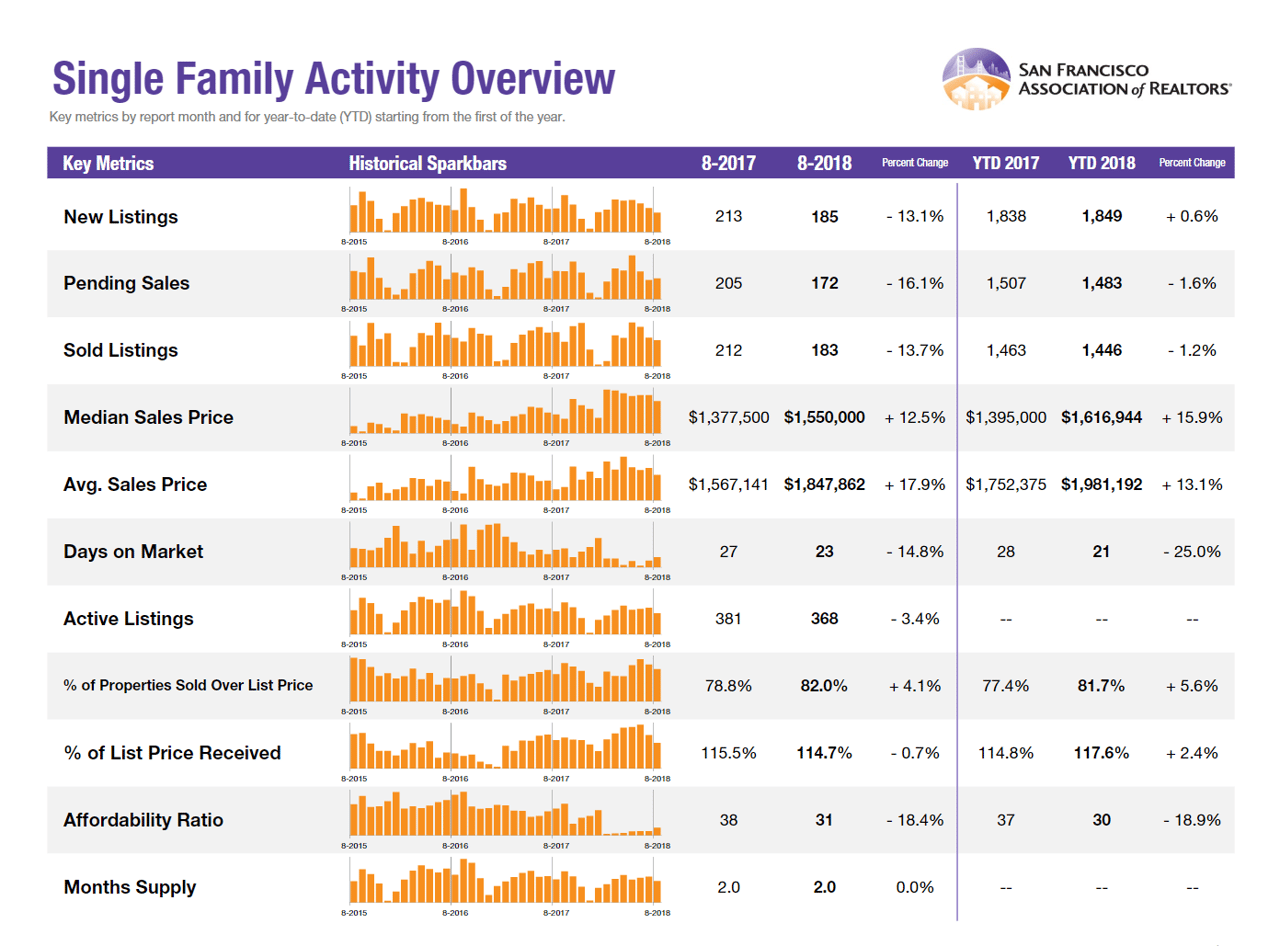

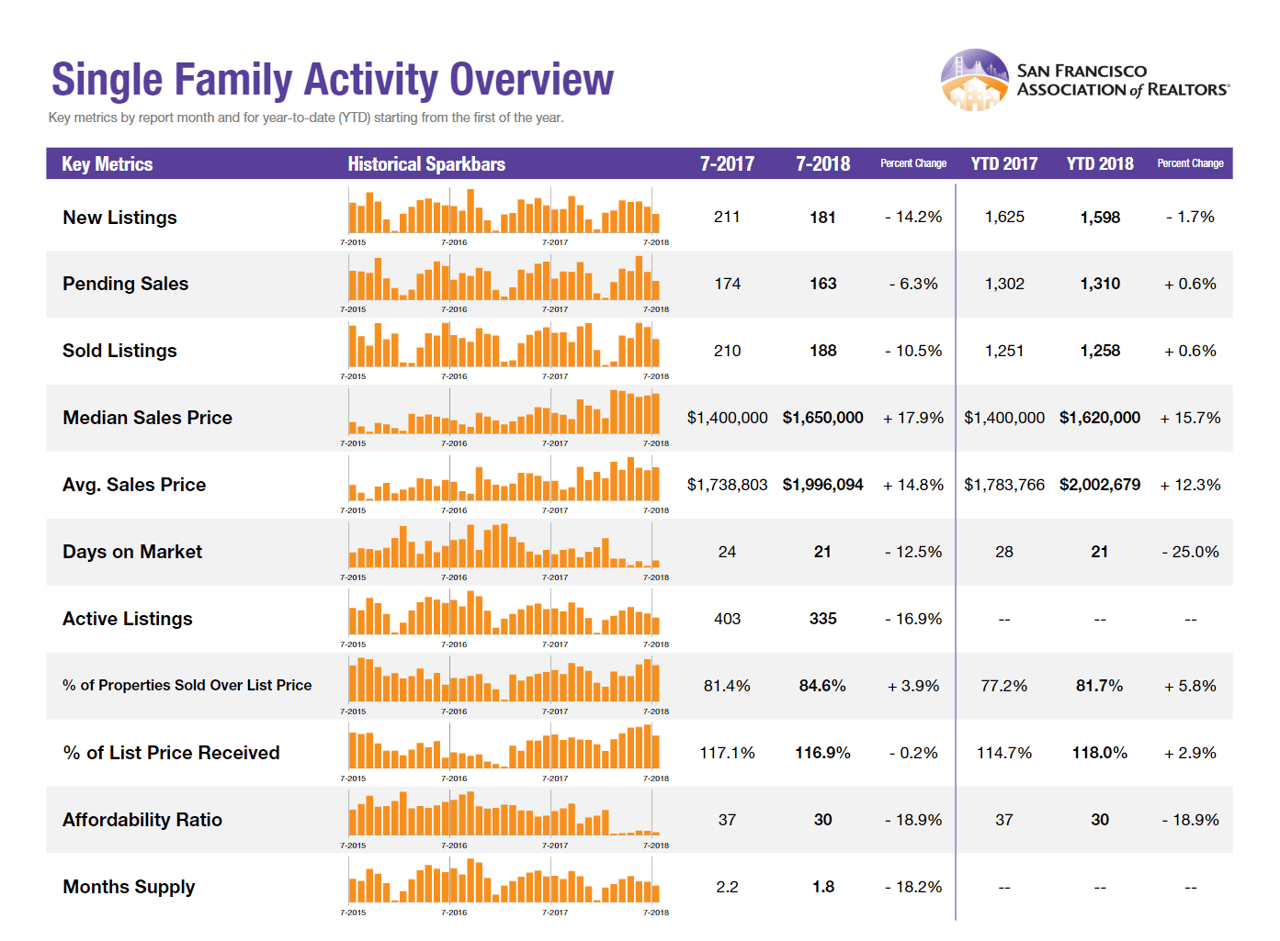

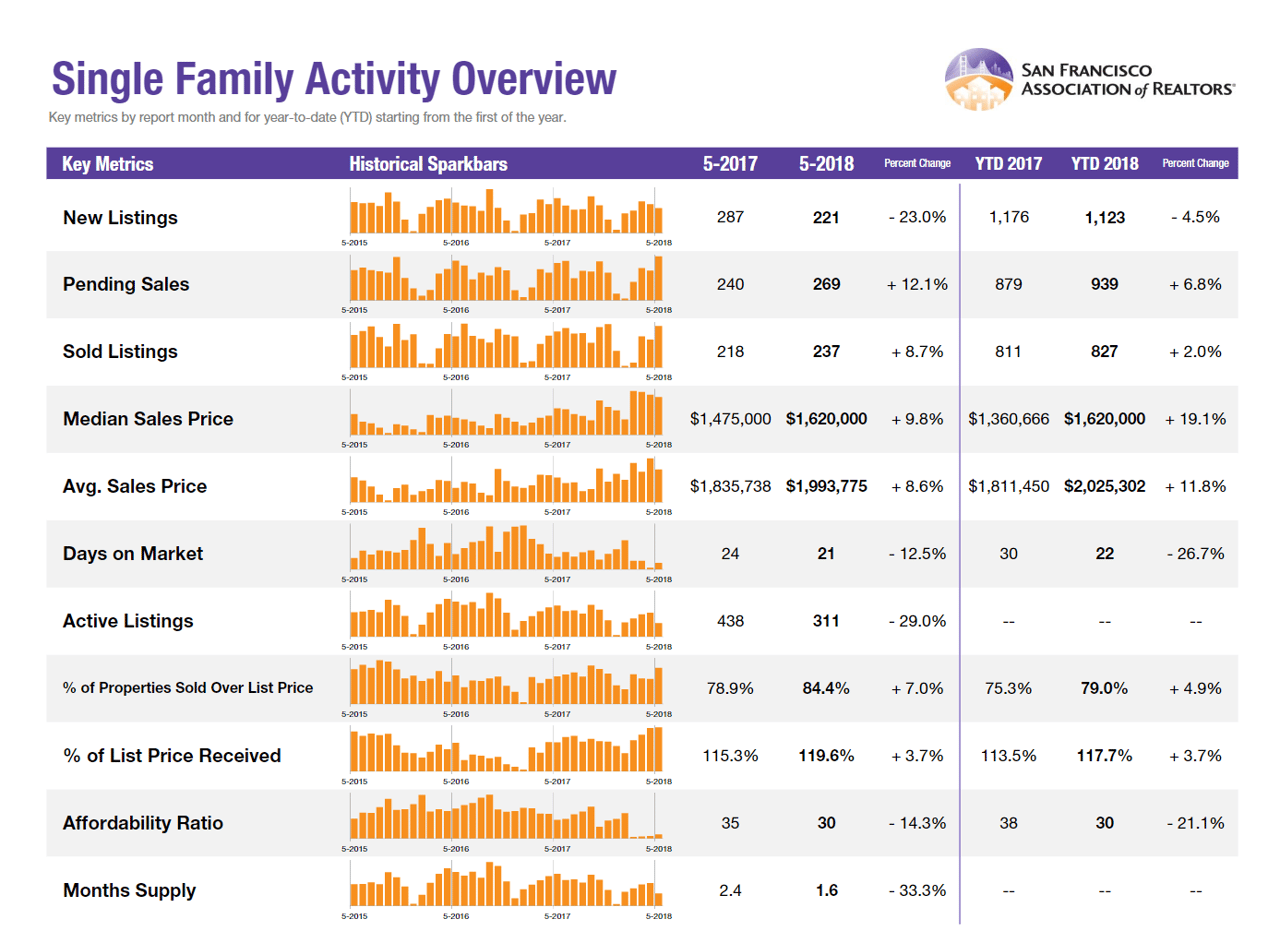

Click here to read the San Francisco report.

Click here to read the North Bay report.

That wraps up this edition. We look forward to sharing more market insights in our next writing, so see you soon!

The Team at Artemis

Disclaimer

NFA / DYOR - Not Financial Advice / Do Your Own Research

Information provided herein is for informational purposes only and is subject to change without notice. This publication does not constitute, either explicitly or implicitly, any services or financial advice by Artemis Real Estate. Information provided is not guaranteed, and Artemis does not guarantee the accuracy of any information obtained from a third party.