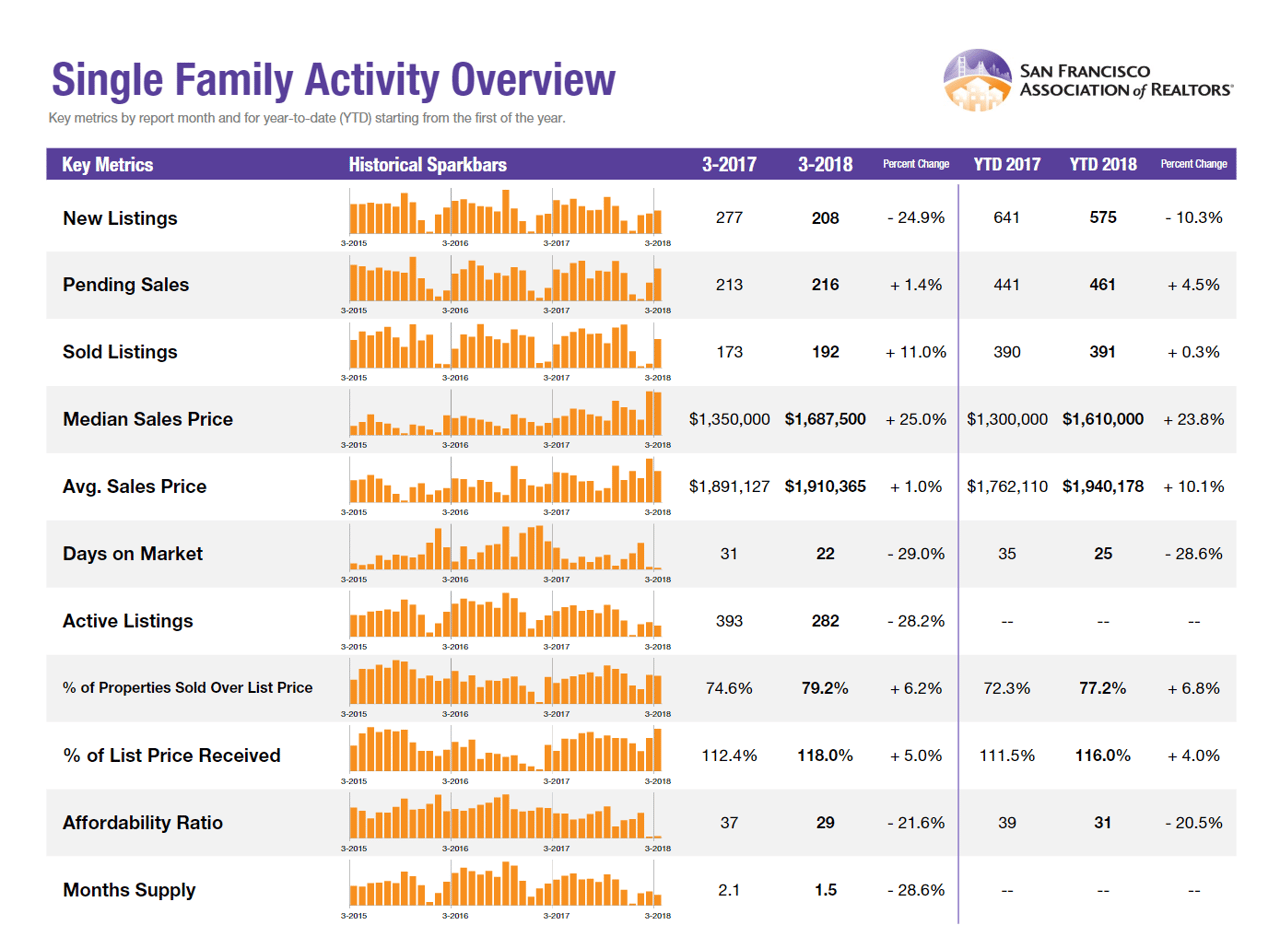

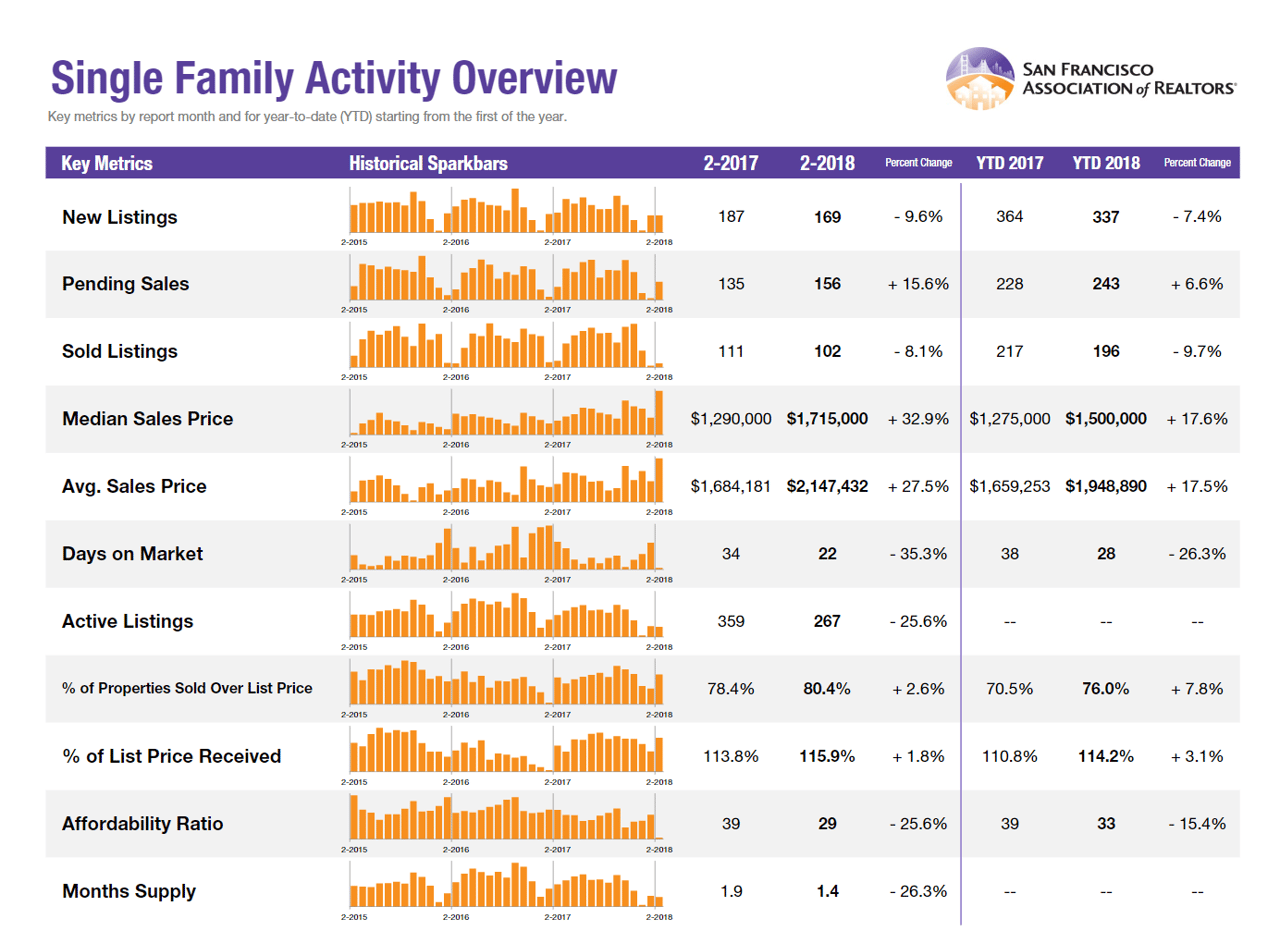

Absorption‐Rates in Key Markets

In this post, we're going to sample different areas, looking for soft spots. We'll use MSI (Months Supply of Inventory) as our barometer.

“Months Supply of Inventory” (MSI) = Active Listings ÷ Properties currently in contract.

-

In contract covers both

-

“Under contract” ➜ offer accepted, contingencies still open, and

-

“Pending” ➜ all contingencies removed, headed to close.

Because a Bay-Area escrow typically runs ±30 days, dividing actives by today’s “in-contract” count gives a 30-day pulse on how quickly inventory is being absorbed right now.

-

Reading the gauge

0 – 3 MSI → fast absorption, sellers dominate

3 – 6 MSI → balanced negotiating table

6 + MSI → slow absorption, buyers gain leverage

Is the Market Lean or Lopsided?

A Snapshot Absorption Tour of San Francisco & Marin — May 2025

1 · San Francisco: City-Wide Pulse

| Segment | Active | In Contract | MSI | Quick Take |

|---|---|---|---|---|

| All property types | 1,168 | 384 | 3.0 | Almost perfectly balanced. |

| Single-family homes | 334 | 168 | 2.0 | Tight; sellers still call the shots. |

| Condos | 686 | 179 | 3.8 | Leaning buyer-friendly. |

2 · Neighborhood Micro-Markets

Single-Family Homes

| Pocket / District | Active | In Contract | MSI | Comment |

|---|---|---|---|---|

| Noe Valley & surrounds (D5) | 52 | 28 | 1.9 | Hottest SFH zone—multiple offers. |

| Lake District / Sea Cliff / Jordan Park | 6 | 3 | 2.0 | Tight, affluent west-of-park niche. |

| Pac Hts / Presidio Hts / Marina / Cow Hollow (D7) | 31 | 5 | 6.2 | Softest city pocket; high-end buyers have leverage. |

Condos

| Pocket / District | Active | In Contract | MSI | Comment |

|---|---|---|---|---|

| Noe Valley & surrounds (D5) | 53 | 29 | 1.8 | Mirrors SFH heat. |

| Eureka Valley / Dolores Hts (D5-K) | 9 | 9 | 1.0 | Sold out before the sign’s up. |

| Pac Hts / Marina / Cow Hollow (D7) | 52 | 22 | 2.3 | Condos outperform neighboring houses. |

3 · Marin County Roll-Up

| Scope & Property Type | Active | In Contract | MSI | Pulse |

|---|---|---|---|---|

| County-wide (all types) | 628 | 196 | 3.2 | Neutral. |

| Single-family only | 462 | 152 | 3.0 | Mirrors macro balance. |

Marin Sub-Markets — Single-Family Only

| Area | Active | In Contract | MSI | Temperature |

|---|---|---|---|---|

| Ross Valley + Larkspur/Corte Madera | 113 | 48 | 2.3 | Seller-leaning, especially turnkey. |

| Mill Valley | 57 | 22 | 2.6 | Slightly looser but still brisk. |

| Belvedere & Tiburon | 54 | 10 | 5.4 | Softest Marin pocket; luxury slowing. |

| Belvedere & Tiburon Condos | 12 | 1 | 12 | Buyers firmly in control |

4 · Ultra-Luxury Snapshot — $5 Million+ Single-Family Homes

| Market | Active | In Contract | MSI | Reality Check |

|---|---|---|---|---|

| San Francisco $5 M+ | 43 | 6 | 7.1 | Deep buyer leverage; patience or price cuts required. |

| Marin $5 M+ | 65 | 4 | 16.3 | Inventory tsunami. Sellers need strategy, staging, and serious pricing discipline. |

What It Means for You

| If you’re a… | Playbook right now |

|---|---|

| Buyer (High-end D7 SFH or $5 M+ in Marin/SF) | Negotiate: 7–16 MSI equals pricing power, inspection windows. |

| Buyer (Noe, Eureka, Mill Valley core) | Pre-underwrite and pounce. Short contingencies or more likely, none. |

| Seller (Hot pockets ≤ $5 M) | List polished and priced at market to ignite multiple offers; hesitation can slide you from 2 MSI into neutral fast. |

| Seller (Soft pockets or ultra-luxury) | Lean on data-driven pricing, global marketing, and patience. Consider strategic concessions early to stand out. |